I'm watching the markets and trying to gain a grasp of what the market is doing and how our abilities to adapt as well as the changes in the market due to the pandemic impact our export abilities. This is a blog post so I'm not going to justify everything I say or use citations for a basic discussion. However, the information presented is based in solid logic and in general research support. What I am mostly interested in is the connection of pre-markers that signal a fundamental change in the economy that would hint at a specific type of recovery.

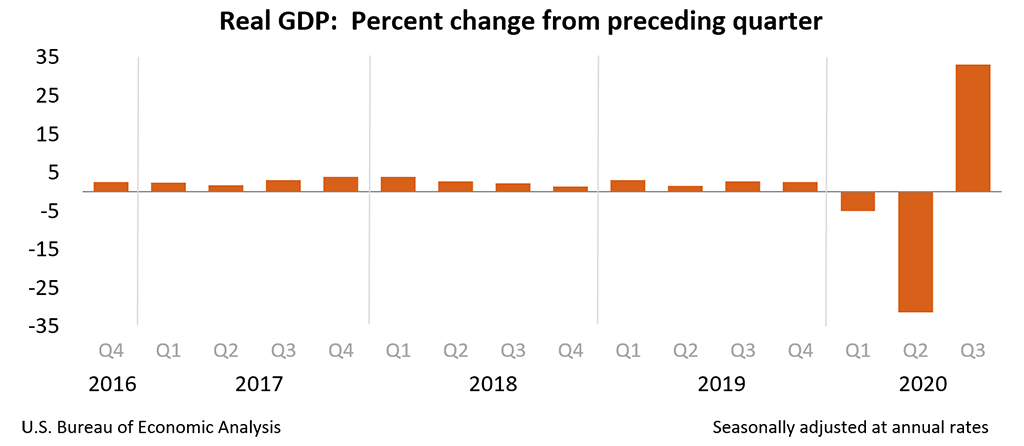

The Bureau of Economic Analysis (BEA) provides information and data for public consumption. It is important for governments to provide this type of information so that companies, investors, intellectuals, etc... can try and make meaning out of the information for business decision making as well as gauge our current economic health. The BEA came out with some powerful GDP improvements in Q3 2020 mounting to a 33.1% increase.

The Bureau of Economic Analysis provides the following explanation...."

The increase in real GDP reflected increases in personal consumption expenditures (PCE), private inventory investment, exports, nonresidential fixed investment, and residential fixed investment that were partly offset by decreases in federal government spending (reflecting fewer fees paid to administer the Paycheck Protection Program loans) and state and local government spending. Imports, which are a subtraction in the calculation of GDP, increased (table 2)."

The IMF seemed low as a benchmark for the U.S. so my argument is that it will likely be much higher than expected based on the uniqueness of the economy as having a number of central supply chain hubs. I wrote a little article about how I think they were a little low and there might be a different projection for the U.S.

What the IMF is Right and Wrong About on their Economic Projections for the U.S.? A boost in GDP may also create a little more investment rip environment.

Based on the theoretical assumptions I have been working off of, I believed that Q3 and Q4 are likely to be strong quarters. It is an adaption kind of concept with a little chaos theory mixed in. It is important to remember that all economics is the measurement of human activity regardless of the currency or measurements we use. Thus, we must understand human behavior and financial behavior to better understanding of the market and how they interplay to create improvements/declines.

You can read a bout a few of these projections.

GDP Contracts 1st Q of 2020-Is It a Short Lived Shock and Digital GDP Recovery? After the first major economic contraction we found that the fundamentals of the society stayed the same and he investment markets were strong. We can also see this in the Q3 BEA statistics that are showing how there is money that can be used for investment, purchases, and general capital availability that move beyond government stimulus.

While we have some indication that exports are improving there doesn't appear to be as much movement there as there was in GDP improvement. What we might want to watch is Q4 GDP numbers and if by the beginning of the Q4 if we will see a bump in exports as well. Many nations are beginning to think about post-COVID life and a number of companies/people may have delayed purchases which could be realized if we see sales in heavy equipment and inventory (as a precursor to purchases).

No idea if it will happen. So far it seems to be fairly close to projections. I'm not a career economist just a person with advance degrees in business and significant economic understandings.

No comments:

Post a Comment